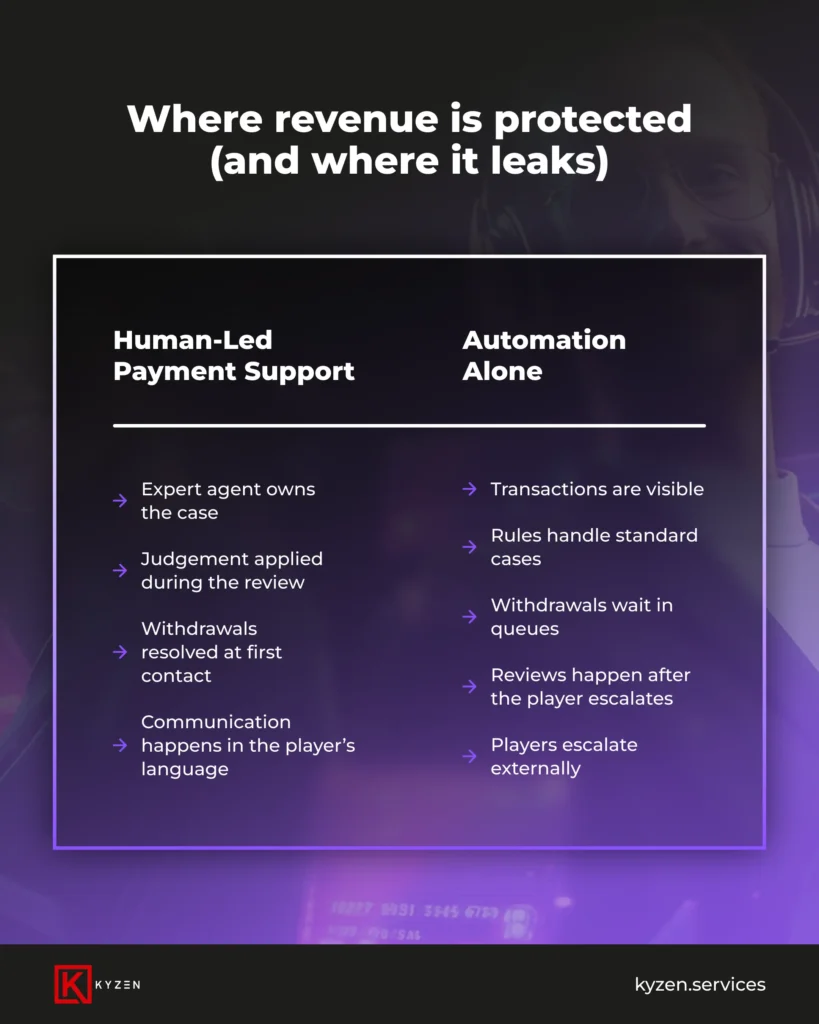

Payment tools handle routing, fallbacks, and method optimization. Human agents make the judgement calls that protect trust when a withdrawal enters review, a VIP needs clarity, or accountability is required.

That is where player relationships weaken and potential NGR starts to leak over time. Most operators do not see it until a high-value account goes quiet or the dispute rate climbs without a clear cause.

Placing clear ownership and informed communication at that moment separates operators who protect potential NGR from those who react only after impact is visible.

When withdrawal issues are not resolved early, they escalate into formal disputes.

Every Flagged Withdrawal Needs a Judgement Call

Payment orchestration platforms like PaymentIQ give operators visibility across the transaction flow. Routing logic, fallback rules, and transaction performance data by market, all of it is available inside the platform. That is exactly what it was built to do.

What it cannot do is read a withdrawal review, understand the regulatory context behind it, and communicate a resolution to the player in their language. That is a human call, and how it is handled often decides whether confidence holds or breaks.

When reassurance is missing, the player does not wait. They contact their bank and the case moves from a support ticket to a formal dispute. One that is far harder to recover.

Informed decision making during withdrawal reviews is what keeps the relationship intact.

This is where operational ownership matters most:

- The ability to read a compliance-driven review status and act on it directly.

- Identifying when a PSP decline warrants a fallback route or a player-facing explanation, and flagging it for action.

- The judgement to identify a risk-flagged behaviour pattern and decide the appropriate response.

Local Expertise Is What Regulated Markets Actually Demand

Regulated markets impose payment and compliance constraints that vary sharply by jurisdiction. In markets like Germany and Brazil, limits, KYC checks, and transaction controls are enforced automatically through platform and regulatory frameworks.

German players operate under GGL oversight with a strict EUR 1,000 monthly deposit limit applied across all licensed operators. In Brazil, Pix flows and CPF verification are system enforced, with compliance rules differing materially from European markets.

When a withdrawal review opens in either market and player contact is required, the explanation must be clear, accurate, and delivered in the player’s language.

Clear, market fluent communication at that point keeps the review moving and protects player confidence.

VIP Escalations Are Not a Queue Problem

High-value players drive a large share of operator revenue. Their tolerance for uncertainty during withdrawals is low, especially when clear answers are missing.

When a withdrawal review opens on a VIP account, the resolution window is short.

At this stage, review context, visibility, and decision authority sit with the Risk, Payments, and Fraud function.

These players need:

- Full context on the VIP account and the withdrawal review.

- Clear visibility into what is driving the review status.

- Defined authority on next steps and timely communication of outcomes.

When execution across review, approval, and communication is poorly aligned, delays compound and confidence erodes. When handoffs are tight and accountability is clear, VIP escalations resolve within the window that still protects the relationship.

Where Internal Handoffs Create Revenue Risk

Fragmented team ownership is where NGR quietly leaks.Even with Risk, Payments, and Fraud involved from the start, unclear sequencing across reviews and approvals can stall a withdrawal for hours. By the time clarity arrives, the player has often already made a decision.

This pattern shows up consistently in operations that have grown around individual functions rather than around the full transaction lifecycle. The consequences are measurable:

- Withdrawal review times extend across markets as cases change hands.

- Extended review times increase the rate at which players file formal disputes.

- Dispute ratios that trend toward Visa or Mastercard monitoring thresholds can lead to scheme-level scrutiny and restrictions over time.

KYZEN Functions as the Operational Backbone Operators Need at Scale

Operators who protect NGR as complexity grows pair strong payment infrastructure with clear operational ownership across the withdrawal lifecycle.

Within KYZEN’s operating model, payment reviews and escalation decisions sit with Risk, Payments, and Fraud teams, while multilingual Customer Support and VIP teams handle player communication when required.

These functions operate in a coordinated flow, with transaction records, review status, and decision inputs remaining visible throughout the case lifecycle. This ensures operational judgement is applied during payout reviews, not after player confidence has already weakened.

When player facing teams have visibility into transaction records and review status, communication stays accurate and timely. Final decisions remain with Risk, Payments, and Fraud, but unnecessary back and forth is removed. That coordination is what turns payment support from a cost function into a retention engine.